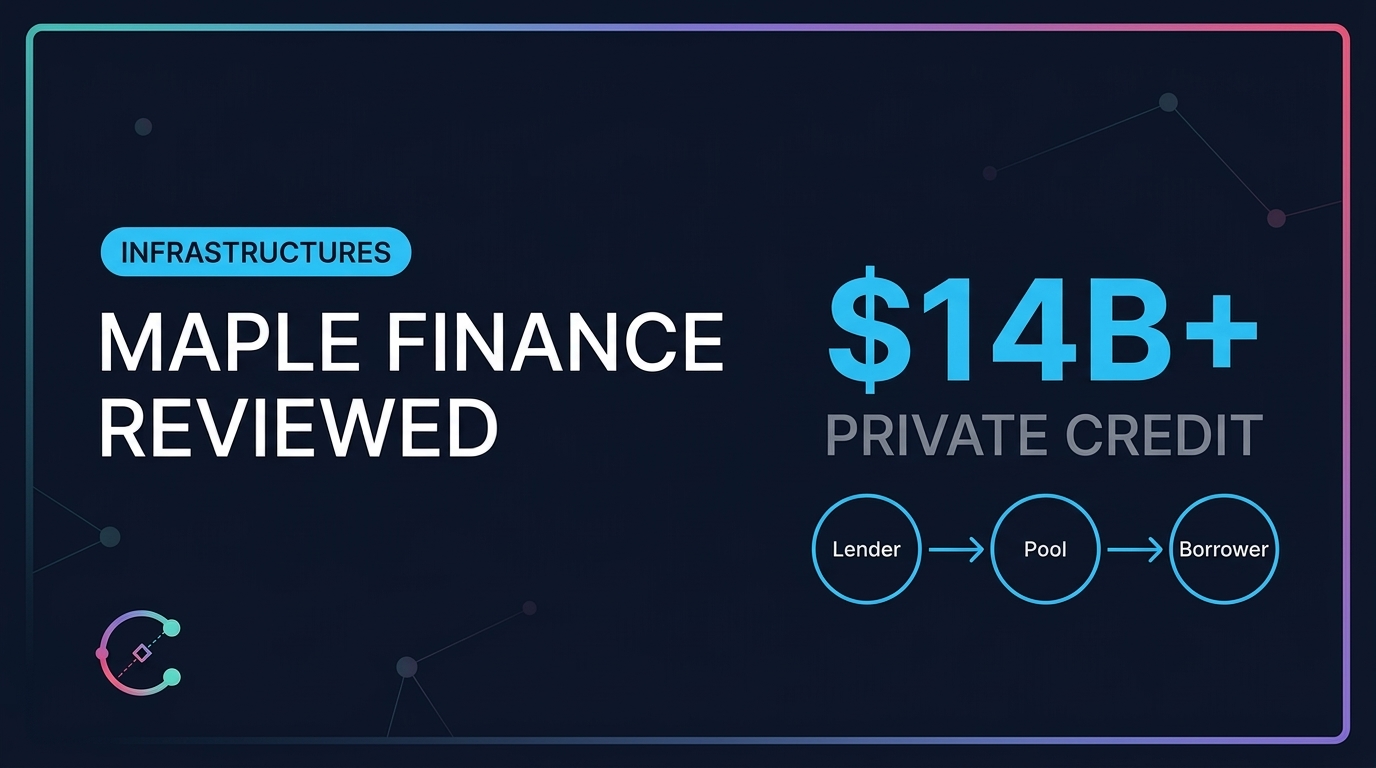

Maple Finance Review: How Tokenized Private Credit Works On-Chain

Maple Finance has established itself as one of the leading platforms for tokenized private credit, connecting institutional borrowers with on-chain lenders through products like SyrupUSDC and SyrupUSDT. In a market where tokenized treasuries dominate the conversation, Maple Finance occupies a different and arguably more consequential position: it brings the $1.7 trillion private credit market on-chain, offering yields that significantly exceed what government debt products provide. The platform has facilitated over $14 billion in cumulative loan origination since launch, making it one of the highest-volume protocols in the real world asset space.

This Maple Finance review covers how the platform works, what products it offers, who borrows through it, what yields lenders can expect, and what risks investors must evaluate before committing capital. Whether you are an institutional lender evaluating on-chain credit opportunities or a retail investor considering higher-yield alternatives to tokenized treasuries, this analysis provides the data and context required for an informed decision.

What Is Maple Finance and How Does It Work?

Maple Finance is a decentralized credit protocol that facilitates institutional lending and borrowing on-chain. The platform operates as a marketplace where institutional borrowers, primarily crypto trading firms, market makers, and fintech companies, access capital from lenders who deposit stablecoins into lending pools. Pool delegates, who are professional credit managers vetted by Maple Finance, underwrite the loans, set terms, and manage the credit risk on behalf of depositors.

The mechanics distinguish Maple Finance from both traditional private credit and from other DeFi lending protocols. Unlike Aave or Compound, which rely on overcollateralized lending where borrowers must deposit more collateral than they borrow, Maple Finance facilitates undercollateralized or partially collateralized lending based on the creditworthiness of institutional borrowers. This model mirrors traditional private credit but executes on blockchain infrastructure, which provides transparency into loan terms, repayment schedules, and pool performance that traditional private credit lacks.

The protocol operates on Ethereum and Solana, with the majority of its total value locked deployed on Ethereum. Maple Finance has evolved significantly since its early days, when a series of borrower defaults in late 2022 exposed weaknesses in its credit underwriting process. The platform restructured its operations, improved its due diligence standards, and launched new products that have driven the recovery and growth of its lending volumes through 2025 and 2026.

Maple Finance Products: SyrupUSDC and Lending Pools

SyrupUSDC: The Retail-Accessible Yield Product

SyrupUSDC is Maple Finance’s flagship retail product, designed to offer lenders exposure to institutional private credit yields through a simple deposit mechanism. Lenders deposit USDC into the SyrupUSDC vault and receive syrupUSDC tokens in return. These tokens accrue yield from the underlying lending activity, with the token price increasing daily to reflect earned interest. The current annualized yield on SyrupUSDC is approximately 8% to 12%, depending on market conditions and borrower demand.

The yield premium over tokenized treasuries is substantial. While products like BUIDL and OUSG offer approximately 4.5% from US government debt, SyrupUSDC delivers roughly double that return by lending to institutional borrowers who pay higher interest rates for the convenience and speed of on-chain capital access. This yield premium compensates lenders for the higher credit risk inherent in private lending compared to government-backed securities.

SyrupUSDC has a minimum deposit of approximately $100, making it accessible to retail investors who want exposure to tokenized private credit without meeting the institutional minimums that traditional private credit funds require. The product operates on Ethereum and has attracted significant capital inflows as investors seek higher yields in a market where treasury rates, while attractive, are below what private credit can offer.

Institutional Lending Pools

Beyond SyrupUSDC, Maple Finance operates dedicated institutional lending pools that serve specific borrower segments and risk profiles. These pools are managed by professional pool delegates who specialize in particular credit markets. The Cash Management Pool focuses on short-duration, low-risk lending to top-tier institutional borrowers. The High Yield Pool targets higher-returning opportunities with correspondingly higher risk tolerance.

Institutional lending pools on Maple Finance typically require larger minimum deposits and may involve KYC requirements, depending on the pool delegate’s policies. The yields in these pools range from 6% to 15% annually, with the variation reflecting differences in borrower credit quality, loan duration, and collateralization levels. Pool delegates provide regular reporting on loan performance, borrower health, and pool composition, giving lenders visibility into the credit risk they are taking.

Who Borrows Through Maple Finance?

Understanding who borrows through Maple Finance is essential for evaluating the credit risk that lenders assume. The platform’s borrower base consists primarily of institutional crypto-native firms that need short-to-medium term capital for trading operations, market making, and treasury management.

The largest borrower categories include crypto trading firms and market makers who use borrowed capital to fund trading positions and provide liquidity across centralized and decentralized exchanges. These firms generate revenue from trading spreads and arbitrage opportunities, and they borrow on Maple Finance because on-chain lending provides faster access to capital than traditional lending relationships, often with funding available within 24 to 48 hours compared to weeks for traditional credit facilities.

Fintech companies and digital asset service providers also borrow through Maple Finance to fund working capital needs, bridge financing gaps, and manage treasury operations. Some borrowers use Maple Finance loans to fund real-world activities outside the crypto ecosystem, effectively using on-chain capital markets to access credit that traditional banks may not provide at competitive rates or speed.

Maple Finance conducts due diligence on all borrowers through its pool delegate structure. Delegates evaluate borrower financials, trading strategies, risk management practices, and collateral arrangements before approving loans. This underwriting process has been significantly strengthened since the platform’s 2022 default events, with more rigorous credit assessment standards, enhanced monitoring, and faster intervention mechanisms when borrower health deteriorates.

Yield Analysis: Why Maple Finance Pays More Than Treasuries

The yield premium that Maple Finance offers over tokenized treasuries reflects the fundamental difference between government credit risk and private credit risk. US Treasury securities carry the full faith and credit of the US government, which is considered the lowest-risk credit in the world. Private borrowers on Maple Finance, regardless of their institutional quality, carry credit risk that exceeds government debt. The higher yield compensates lenders for this additional risk.

Current yields on Maple Finance products range from approximately 8% to 12% for SyrupUSDC and 6% to 15% for institutional pools. These returns compare favorably to traditional private credit funds, which typically offer 8% to 14% net returns but require minimum investments of $250,000 or more and impose multi-year lock-up periods. Maple Finance delivers comparable yields with lower minimums and shorter lock-up terms, although with different risk characteristics.

The yield is generated from interest payments made by borrowers on their loans. Maple Finance takes a protocol fee, pool delegates take a management fee, and the remaining interest flows to lenders. The fee structure is transparent and visible on-chain, which is a significant advantage over traditional private credit funds where fee transparency is often limited. For investors comparing yield options, our analysis of tokenized treasuries compared provides the baseline against which Maple Finance yields should be evaluated.

Risks of Lending Through Maple Finance

Maple Finance carries risks that are materially different from and generally higher than those associated with tokenized treasury products. Understanding these risks is essential before committing capital, particularly for investors whose primary experience is with lower-risk yield products.

Credit and Default Risk

The most significant risk on Maple Finance is borrower default. If a borrower fails to repay their loan, lenders may lose part or all of their deposited capital. Maple Finance experienced this directly in late 2022 when several borrowers, including entities connected to the FTX collapse, defaulted on loans totaling approximately $54 million. These defaults resulted in real losses for lenders who had capital in the affected pools.

Since those events, Maple Finance has strengthened its credit underwriting processes, reduced concentration risk by diversifying across more borrowers, and implemented faster liquidation mechanisms for collateral. However, credit risk cannot be eliminated in undercollateralized lending. Lenders on Maple Finance are functioning as private credit providers, and they bear the credit risk that comes with that role.

Smart Contract and Protocol Risk

Maple Finance operates through smart contracts that manage deposits, loan disbursements, interest accrual, and repayments. Vulnerabilities in these contracts could potentially result in loss of funds, frozen withdrawals, or incorrect interest calculations. The protocol’s smart contracts have been audited by multiple firms, but audit coverage does not guarantee the absence of vulnerabilities. The complexity of Maple Finance’s pool delegation and credit management logic creates a larger attack surface than simpler DeFi protocols.

Liquidity Risk

Withdrawing capital from Maple Finance lending pools is not always instant. While some pools offer relatively quick withdrawal windows, others may impose lock-up periods or withdrawal queues when outstanding loans have not yet matured. If all lenders attempt to withdraw simultaneously, the pool may not have sufficient liquid capital to honor all requests immediately. Lenders should understand the withdrawal terms for their specific pool before depositing and should not deposit capital they may need on short notice.

Maple Finance vs Competitors in On-Chain Credit

Maple Finance competes with several platforms in the tokenized private credit space. Centrifuge, which focuses on tokenizing real-world receivables and trade finance, serves a different borrower segment but competes for the same lender capital. Goldfinch targets emerging market lending, connecting DeFi capital with borrowers in developing economies. Credix focuses on Latin American credit markets.

Maple Finance differentiates through its focus on institutional crypto-native borrowers, its pool delegate model for professional credit management, and its retail-accessible SyrupUSDC product. The platform’s scale, with over $14 billion in cumulative origination, exceeds most competitors. However, the concentration of borrowers in the crypto trading sector means that Maple Finance’s performance is more correlated with crypto market conditions than platforms like Centrifuge that serve non-crypto borrowers.

For investors building a diversified on-chain credit portfolio, combining Maple Finance exposure with allocations to Centrifuge (real-world receivables) and tokenized treasuries creates a more balanced risk profile than concentrating in any single platform. Our guide on how to buy tokenized assets covers the broader platform landscape for investors evaluating their options. The $14 billion on-chain private credit market provides additional context on how Maple Finance fits within the broader tokenized credit ecosystem.

Frequently Asked Questions

What is Maple Finance?

Maple Finance is a decentralized credit protocol that connects institutional borrowers with on-chain lenders. It facilitates undercollateralized lending through professionally managed lending pools, offering yields of 8% to 12% through products like SyrupUSDC that are accessible to both retail and institutional investors.

What yield does Maple Finance offer?

SyrupUSDC currently offers approximately 8% to 12% annualized yield. Institutional lending pools range from 6% to 15% depending on borrower quality, loan duration, and collateralization. These yields significantly exceed tokenized treasury returns of approximately 4.5%.

Is Maple Finance safe?

Maple Finance carries higher risk than tokenized treasuries. The platform experienced borrower defaults in 2022 resulting in approximately $54 million in losses. Since then, underwriting standards have been strengthened, but credit risk, smart contract risk, and liquidity risk remain. Only invest capital you can afford to lose.

How does Maple Finance differ from Aave or Compound?

Aave and Compound use overcollateralized lending where borrowers deposit more collateral than they borrow. Maple Finance facilitates undercollateralized lending to institutional borrowers based on creditworthiness, offering higher yields but with credit default risk that overcollateralized protocols do not carry.

What is SyrupUSDC?

SyrupUSDC is Maple Finance’s retail-accessible yield product. Lenders deposit USDC and receive syrupUSDC tokens that accrue yield from institutional lending activity. The minimum deposit is approximately $100, and yields currently range from 8% to 12% annually depending on market conditions.

The Bottom Line

Maple Finance occupies a unique position in the tokenized asset market. While most attention focuses on tokenized treasuries and their government-backed safety, Maple Finance brings the private credit market on-chain, offering yields that are roughly double what Treasury products provide. The platform’s $14 billion in cumulative origination demonstrates that institutional borrowers value the speed and efficiency of on-chain credit, and the launch of SyrupUSDC has made these yields accessible to a broader investor base.

The risks are real and should not be minimized. The 2022 default events demonstrated that undercollateralized lending carries genuine credit risk, and lenders on Maple Finance are functioning as private credit providers whether they recognize that role or not. The platform has improved its underwriting and risk management since those events, but the fundamental risk profile of private lending remains higher than government debt.

For investors who understand and accept this risk profile, Maple Finance offers one of the most compelling yield opportunities in the on-chain economy. The combination of institutional-grade borrowers, professional pool delegation, transparent on-chain reporting, and retail-accessible minimums creates a product category that did not exist before blockchain infrastructure made it possible. Subscribe to the Commodara newsletter for ongoing coverage of on-chain credit markets and the platforms that power them.