SPV Tokenization: How to Structure the Legal Entity Behind Your Token

SPV tokenization is the legal foundation of nearly every compliant token offering, because the special purpose vehicle is what holds the underlying asset and issues the tokens that represent it. Without a properly structured SPV, a tokenized product has no legal connection between the digital token on the blockchain and the real-world asset it claims to represent. The SPV is the bridge that gives the token its legal meaning, its enforceability, and its value.

This guide walks asset owners through the complete SPV tokenization process: what an SPV is, why it matters for tokenized offerings, how to choose the right jurisdiction, how to structure the entity for different asset classes, and how to connect the legal entity to the smart contract that governs the token. Whether you are tokenizing a commercial property, a private credit portfolio, or a fund structure, the SPV is where the legal and technical layers of your project meet.

What Is SPV Tokenization?

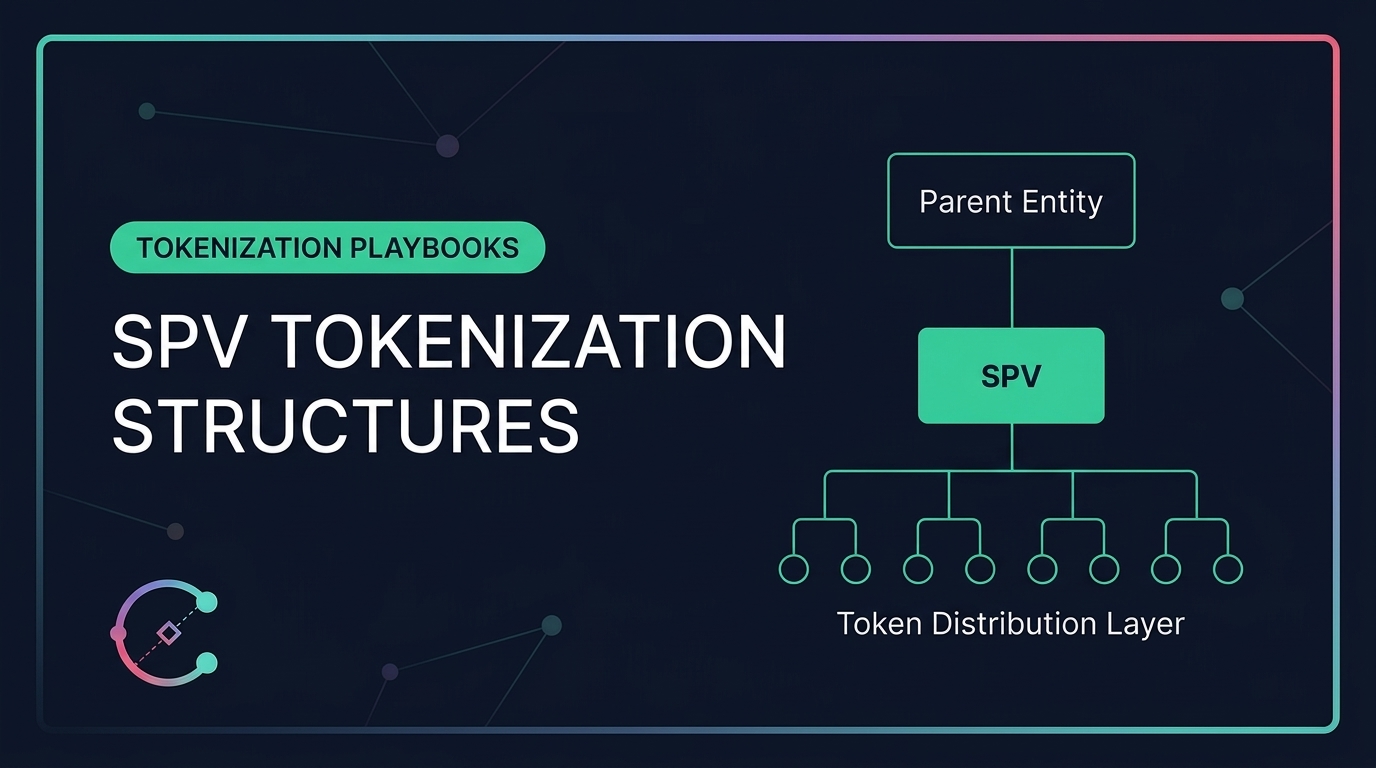

A special purpose vehicle is a legal entity created for a single, defined purpose. In the context of SPV tokenization, that purpose is to hold a specific asset or pool of assets and issue digital tokens that represent fractional ownership or claims on that entity. The SPV sits between the asset and the investor: it owns the asset, and the investor owns tokens that represent shares in the SPV.

This structure is not unique to blockchain. SPVs have been used in traditional finance for decades in securitization, project finance, and real estate syndications. What makes SPV tokenization different is that the ownership records, transfer restrictions, and distribution mechanics are encoded in a smart contract on a blockchain rather than managed through paper documents and centralized registries. The legal entity remains traditional; the ownership layer becomes programmable.

The practical result is that an asset owner can create an SPV, transfer a $20 million commercial property into it, and issue 200,000 tokens at $100 each, where each token represents a 0.0005% ownership stake in the SPV. Token holders receive proportional distributions of rental income through the smart contract, and their ownership is recorded immutably on the blockchain. The SPV’s operating agreement governs the rights and obligations of all parties, while the smart contract automates the mechanics of ownership transfer and income distribution.

Why SPVs Are Necessary for Tokenized Offerings

An SPV is necessary for SPV tokenization because most assets cannot be directly divided and transferred on a blockchain. You cannot split a building into pieces and put each piece on Ethereum. What you can do is create a legal entity that owns the building and then tokenize shares of that entity. The SPV provides the legal wrapper that makes fractional ownership enforceable in a court of law.

Without an SPV, a token is just a number on a blockchain with no legal significance. A buyer of that token has no legal claim on any asset, no right to any income, and no legal recourse if something goes wrong. The SPV gives the token its legal substance by establishing a clear chain of ownership: the SPV owns the asset, the token represents a share of the SPV, and the token holder’s rights are defined in the SPV’s governing documents.

The SPV also provides bankruptcy remoteness. If the asset owner’s primary business fails, the assets held in the SPV are protected from the owner’s creditors because the SPV is a separate legal entity. This protection is critical for investor confidence. No institutional investor will participate in a tokenized offering where the underlying asset could be seized to satisfy the issuer’s unrelated debts. SPV tokenization structures that provide genuine bankruptcy remoteness are a prerequisite for attracting institutional capital.

Choosing the Right Jurisdiction for SPV Tokenization

The jurisdiction where you form your SPV affects everything from tax treatment to regulatory requirements to investor access. Different jurisdictions offer different advantages for SPV tokenization, and the optimal choice depends on the asset type, the target investor base, and the regulatory framework you need to comply with.

United States: Delaware LLC

The Delaware LLC is the most common SPV structure for tokenized offerings targeting US investors. Delaware’s well-established body of corporate law, its business-friendly Court of Chancery, and its flexible LLC statute make it the default choice for US-based tokenization projects. A Delaware LLC can be structured with a single member (the issuer) or with the token holders as members, depending on the offering structure.

For SPV digital securities offered under Regulation D (accredited investors) or Regulation A+ (qualified with the SEC for broader access), the Delaware LLC provides the legal predictability that securities lawyers and institutional investors require. The operating agreement defines member rights, distribution waterfalls, voting procedures, and transfer restrictions, all of which are then encoded into the smart contract for automated enforcement.

Cayman Islands

The Cayman Islands exempted company is the preferred SPV structure for tokenized fund products targeting international investors. The jurisdiction offers tax neutrality, meaning the SPV itself pays no income tax, corporate tax, or capital gains tax. This tax-neutral status is why most traditional hedge funds and private equity funds are domiciled in the Cayman Islands, and the same logic applies to tokenized fund structures.

BlackRock’s BUIDL fund, the largest tokenized treasury product, uses a Cayman Islands entity as part of its fund structure. The regulatory framework in the Cayman Islands is well understood by institutional investors and their legal counsel, which reduces the due diligence burden compared to less established jurisdictions. For tokenization projects that need to attract global institutional capital, the Cayman Islands remains the standard choice for SPV tokenization.

British Virgin Islands

The British Virgin Islands offers a cost-effective alternative to the Cayman Islands with similar tax neutrality. BVI Business Companies are simpler to form and maintain than Cayman exempted companies, with lower annual fees and less onerous reporting requirements. For smaller tokenization projects or early-stage offerings that do not yet require the full institutional infrastructure of a Cayman structure, the BVI provides a practical starting point.

Singapore and Switzerland

Singapore and Switzerland have emerged as preferred jurisdictions for tokenized offerings that require onshore regulatory compliance in Asia or Europe respectively. Singapore’s Variable Capital Company structure is specifically designed for fund products and has been adopted by several tokenization projects targeting Asian institutional investors. Switzerland’s DLT Act provides a bespoke legal framework for tokenized securities, with the canton of Zug becoming a hub for compliant token issuance. The MiCA regulation framework provides additional pathways for SPV tokenization structures that operate across the European Union.

How to Structure the SPV for Different Asset Classes

The internal structure of your SPV depends on the asset class you are tokenizing. Real estate, private credit, fund products, and commodity-backed tokens each require different legal structures within the SPV to properly represent the rights and obligations of token holders.

Real Estate SPV Tokenization

For real estate tokenization, the SPV typically takes the form of a single-asset LLC or limited partnership that holds title to the property. The SPV’s operating agreement defines how rental income is distributed to token holders, how property expenses are allocated, and how decisions about property management, refinancing, and disposition are made. The complete guide to tokenizing real estate covers the property-specific considerations in detail, but from an SPV perspective, the critical elements are clear title to the property, a defined distribution waterfall, and a governance structure that balances manager authority with token holder rights.

The tokenization entity structure for real estate must also address property-specific liabilities. Environmental liabilities, tenant disputes, and insurance claims should be contained within the SPV so that they do not affect the asset owner’s other properties or businesses. This liability containment is one of the primary reasons for using an SPV rather than tokenizing shares of the asset owner’s primary entity.

Private Credit and Lending SPVs

Private credit SPV tokenization structures are more complex because the SPV acts as both an asset holder and a lending vehicle. The SPV receives capital from token holders, deploys that capital as loans to borrowers, and distributes the interest income back to token holders proportionally. The SPV’s governing documents must define the credit policy, the underwriting standards, the default procedures, and the priority of claims in the event of borrower default.

Tranching is common in private credit SPV tokenization. The SPV issues two or more classes of tokens: senior tokens that receive priority on distributions and have first claim on assets in a wind-down, and junior tokens that absorb losses first but earn higher yields. This tranching structure is familiar to institutional investors from traditional structured credit products and provides risk segmentation that broadens the investor base.

Fund Structure SPVs

Tokenized fund products use SPV structures that mirror traditional fund architecture. A master SPV holds the underlying portfolio assets, and feeder SPVs in different jurisdictions issue tokens to investors in their respective markets. This master-feeder structure allows a single portfolio to serve investors across multiple jurisdictions with different regulatory requirements and tax treatments.

The special purpose vehicle tokenized assets model for funds must comply with investment company regulations in each jurisdiction where tokens are offered. In the US, this typically means relying on exemptions from the Investment Company Act of 1940, such as the Section 3(c)(1) or 3(c)(7) exemptions that limit the number or qualification of investors. The SPV’s offering documents must clearly disclose these regulatory limitations and their implications for token transferability.

Connecting the SPV to the Smart Contract

The legal structure tokenization process requires a clear connection between the SPV’s governing documents and the smart contract that manages the token. This connection is typically established through several mechanisms.

Operating Agreement Provisions

The SPV’s operating agreement or articles of association must explicitly reference the blockchain token as the record of ownership. Provisions should state that the blockchain ledger is the authoritative record of membership interests, that transfers executed through the smart contract constitute valid transfers under the operating agreement, and that distributions made through the smart contract satisfy the SPV’s distribution obligations.

These provisions give the smart contract legal recognition within the SPV’s governance framework. Without them, there is ambiguity about whether a token transfer on the blockchain actually transfers the legal ownership interest in the SPV. Well-drafted provisions eliminate this ambiguity and ensure that the on-chain and off-chain records remain consistent.

Transfer Restrictions and Compliance

Most SPV tokenization offerings involve securities, which means that token transfers must comply with applicable securities regulations. The smart contract must enforce transfer restrictions that match the requirements of the offering exemption. For a Regulation D offering, the smart contract must restrict transfers to verified accredited investors and enforce the typical one-year holding period before resale. For a Regulation S offering, the smart contract must restrict transfers to non-US persons during the distribution compliance period.

These compliance rules are encoded in the smart contract through whitelist mechanisms. Only wallet addresses that have completed KYC/AML verification and investor qualification checks are added to the whitelist, and the smart contract rejects any transfer to a non-whitelisted address. This on-chain compliance enforcement is one of the key advantages of SPV tokenization over traditional fund structures, where compliance is managed manually and transfer restrictions are enforced through paperwork rather than code.

Distribution Mechanics

The smart contract automates the distribution of income from the SPV to token holders. When the SPV generates income, whether from rental payments, interest, dividends, or capital gains, the distribution is executed through the smart contract proportionally to each token holder’s ownership percentage. This automation eliminates the manual processing, calculation errors, and delays that are common in traditional fund administration.

The smart contract must also handle tax withholding where required. For US-source income distributed to non-US token holders, the SPV may be required to withhold taxes at specified rates. The smart contract can automate this withholding based on the investor’s jurisdiction as recorded in the compliance database, ensuring that the SPV meets its tax obligations without manual intervention.

SPV Tokenization Costs and Timeline

Understanding the costs and timeline for SPV tokenization helps asset owners plan their projects realistically and budget appropriately.

Formation and Legal Costs

The cost of forming an SPV for tokenization varies by jurisdiction and complexity. A basic Delaware LLC can be formed for under $1,000 in state fees, but the legal documentation required for a tokenized offering, including the operating agreement, subscription agreement, private placement memorandum, and smart contract legal opinions, typically costs between $50,000 and $200,000 in legal fees depending on the complexity of the offering and the law firm engaged.

Cayman Islands entities carry higher formation costs, typically $5,000 to $15,000 in registration fees plus ongoing annual fees of $2,000 to $5,000. Legal documentation costs are comparable to Delaware structures. For organizations assessing whether the investment is justified for their specific situation, the Commodara Tokenization Readiness Tool provides a structured evaluation that identifies the optimal structure and estimates the associated costs.

Timeline

A typical SPV tokenization project from initial planning to token issuance takes three to six months. The first month is typically spent on legal structuring: choosing the jurisdiction, drafting the SPV documents, and defining the token economics. The second and third months focus on platform selection, smart contract development, and compliance infrastructure setup. The final one to two months cover investor onboarding, regulatory filings if required, and the actual token issuance.

This timeline assumes that the underlying asset is already identified and that the asset owner has engaged experienced legal counsel and a tokenization platform. Projects that require asset acquisition, complex regulatory approvals, or custom smart contract development may take significantly longer. For organizations with tight timelines or unique requirements, a paid consultation with Commodara’s advisory team can help compress the planning phase and avoid common pitfalls.

Frequently Asked Questions

What is SPV tokenization?

SPV tokenization is the process of creating a special purpose vehicle to hold an asset and issuing digital tokens on a blockchain that represent fractional ownership of that SPV. The SPV provides the legal structure that connects the digital token to the real-world asset it represents.

Why do I need an SPV for tokenization?

An SPV is necessary because most assets cannot be directly divided on a blockchain. The SPV holds the asset, and tokens represent shares of the SPV. This structure provides legal enforceability, bankruptcy remoteness, and regulatory compliance that direct tokenization cannot achieve.

Which jurisdiction is best for an SPV tokenization structure?

The best jurisdiction depends on your asset type and target investors. Delaware LLCs are standard for US offerings. Cayman Islands entities suit international fund products. Singapore and Switzerland offer specialized frameworks for Asian and European markets respectively.

How much does SPV tokenization cost?

SPV formation costs range from under $1,000 for a Delaware LLC to $15,000 for a Cayman entity. Legal documentation for a tokenized offering typically costs $50,000 to $200,000 depending on complexity. Platform fees, smart contract development, and compliance infrastructure add additional costs.

How long does SPV tokenization take?

A typical SPV tokenization project takes three to six months from planning to token issuance. This includes one month for legal structuring, two months for platform and smart contract setup, and one to two months for investor onboarding and token issuance.

The Bottom Line

SPV tokenization is the legal infrastructure that makes the entire tokenized asset market possible. Without properly structured SPVs, tokens are nothing more than entries on a blockchain with no legal significance. The SPV provides the legal wrapper, the bankruptcy remoteness, the regulatory compliance, and the governance framework that institutional and retail investors require before committing capital to tokenized products.

The decisions you make about SPV jurisdiction, entity structure, governing documents, and smart contract integration will determine the legal robustness, investor appeal, and regulatory compliance of your tokenized offering. These are not decisions to make without experienced legal counsel and a clear understanding of your asset class, target investor base, and regulatory obligations.

For asset owners evaluating whether their project is ready for SPV tokenization, the Commodara Tokenization Readiness Tool provides a structured assessment of your legal, technical, and market readiness. Subscribe to the Commodara newsletter for ongoing guidance on the legal structures and compliance frameworks that underpin the tokenized economy.