Fractional Ownership Tokenization: How It Works and Where to Start

Fractional ownership tokenization is the process of dividing a high-value asset into smaller digital tokens, allowing multiple investors to own a share of something that was previously accessible only to the wealthy. A $50 million commercial building, a $10 million piece of fine art, or a $500,000 allocation in a private credit fund can be divided into thousands or millions of tokens, each representing a proportional claim on the underlying asset. In 2026, this model is no longer a concept; it is a functioning market with billions of dollars in tokenized assets available to retail and institutional investors across multiple platforms and jurisdictions.

This article explains how fractional ownership tokenization works, which asset classes are available, the platforms enabling access, the legal structures underpinning these products, and the risks that investors must evaluate. Whether you are a first-time investor exploring tokenized products or an experienced allocator looking to diversify into fractional positions, this guide covers the landscape as it stands today.

Table of Contents

This guide begins with how fractional ownership tokenization works and the technology behind it. It then covers which asset classes support fractional ownership and profiles the leading platforms. The following sections examine why this model matters for investors, the legal structures that make it possible, the risks and limitations to evaluate, and how to get started.

What Is Fractional Ownership Tokenization?

Fractional ownership tokenization combines two concepts that have existed independently for decades. Fractional ownership, the idea that multiple people can co-own a single asset, has existed in real estate syndications, limited partnerships, and mutual funds for generations. Tokenization, the process of representing rights on a blockchain, has matured since 2020 into a production-grade technology used by institutions including BlackRock, Franklin Templeton, and JPMorgan.

When these two concepts merge, the result is a system where an asset is held by a legal entity, typically a special purpose vehicle, and digital tokens representing fractional shares of that entity are issued on a blockchain. Each token encodes the holder’s proportional ownership, their right to income distributions like rent or interest, and the compliance rules governing who can hold and transfer the token. The blockchain serves as the ledger of record for ownership, replacing paper certificates and centralized registries with a transparent, programmable, and auditable system.

The practical result is that an investor can gain exposure to a $30 million office building in Manhattan by purchasing a single token for $100. That token represents a fractional claim on the building’s rental income and appreciation, enforced by the smart contract and the legal structure behind it. This is the core value proposition of fractional ownership tokenization: removing the minimum investment barrier that has historically excluded most investors from premium asset classes.

How Fractional Ownership Differs from Traditional Fund Structures

Fractional ownership tokenization is not the same as buying shares in a REIT or an ETF, although the concepts share surface-level similarities. In a REIT, investors buy shares in a company that owns multiple properties; the investor has no direct claim on any specific asset. In fractional ownership tokenization, each token typically represents a claim on a specific asset or a narrowly defined pool of assets held by a dedicated SPV.

This specificity gives investors more transparency and control. A tokenized fraction of a specific warehouse in Dubai is a fundamentally different product from a share in a REIT that owns 200 properties across 15 countries. The investor knows exactly which asset generates their returns, can verify the asset’s performance through on-chain data, and holds a token that is transferable on secondary markets without requiring the fund manager to process a redemption. The complete guide to tokenized real world assets provides the broader context for how these fractional products fit into the overall tokenized economy.

Asset Classes Available Through Fractional Ownership Tokenization

Fractional ownership tokenization has expanded well beyond its origins in real estate. In 2026, investors can access fractional positions across five major asset categories, each with distinct characteristics, return profiles, and regulatory treatment.

Fractional Real Estate

Real estate remains the most intuitive application of fractional ownership tokenization. Commercial properties, residential developments, and hospitality assets have all been tokenized and fractionalized on platforms like RealT, Lofty, and Propy. In the fractional real estate blockchain model, an SPV holds the property, issues tokens representing shares in the SPV, and distributes rental income proportionally to token holders through smart contracts. The Dubai real estate tokenization market has been particularly active, with multiple large-scale developments offering tokenized fractional ownership to international investors.

The advantage of fractional real estate blockchain models over traditional real estate syndications is threefold. First, minimum investments drop from $50,000 or $100,000 to as little as $50 or $100. Second, ownership transfers happen in minutes rather than weeks, because the blockchain handles settlement and the smart contract enforces compliance checks automatically. Third, investors can verify property performance, occupancy data, and distribution histories on-chain rather than relying solely on quarterly reports from a fund manager.

Fractional Treasury and Fixed Income Products

Tokenized treasury products from providers like Ondo Finance, Franklin Templeton, and BlackRock are inherently fractional. An investor can purchase $500 worth of USDY or $20 worth of BENJI and gain exposure to a portfolio of US Treasury bills that traditionally required institutional-scale investments. These products have grown to over $8.7 billion in total value, making them the largest category of tokenized assets by market capitalization.

Fixed income products beyond treasuries, including corporate bonds and structured credit, are also being fractionalized. Platforms like Centrifuge and Goldfinch have pioneered tokenized fractional positions in trade finance and emerging market lending. The yields on these products often exceed what is available through traditional fixed income channels, reflecting both the credit risk of the underlying loans and the efficiency gains from blockchain settlement.

Fractional Private Credit

Private credit has historically required minimum allocations of $250,000 to $1 million. Through fractional ownership tokenization, platforms like Maple Finance and Centrifuge have reduced these minimums to as low as $1,000. SyrupUSDC, Maple’s flagship product, allows investors to earn institutional-grade yields from a diversified pool of borrower loans that have been underwritten through Maple’s credit assessment process.

Fractional investment crypto products in the private credit space offer yields that typically range from 8% to 15% annually, significantly higher than tokenized treasuries but with correspondingly higher risk. The borrower default risk, platform risk, and smart contract risk that come with on-chain lending must be weighed against the yield premium that these products offer.

Fractional Commodities and Alternative Assets

Tokenized gold products like Paxos Gold (PAXG) and Tether Gold (XAUT) allow investors to own fractional shares of physical gold bars stored in regulated vaults. With PAXG, each token represents one troy ounce of gold, but the token can be subdivided to 18 decimal places, meaning an investor can purchase a fraction of an ounce for as little as a few dollars. The tokenized gold market has grown to $5.9 billion in market capitalization with $178 billion in annual trading volume.

Beyond gold, fractional ownership tokenization is being applied to fine art, collectibles, wine, carbon credits, and intellectual property. Platforms like Masterworks have tokenized paintings by Banksy, Basquiat, and Monet, allowing investors to purchase fractional shares of artworks valued at $1 million to $30 million. While these alternative asset categories remain smaller than real estate and fixed income, they demonstrate the breadth of fractional ownership tokenization as a model.

Why Fractional Ownership Tokenization Matters for Investors

The significance of fractional ownership tokenization extends beyond simple access to expensive assets. It represents a structural change in how investment products are designed, distributed, and managed, with implications for portfolio construction, market efficiency, and financial inclusion.

Democratized Access to Premium Asset Classes

The most direct impact of fractional ownership tokenization is the elimination of minimum investment barriers. A retail investor with $1,000 can now build a diversified portfolio across tokenized treasuries, real estate, private credit, and gold that would have required $5 million or more through traditional channels. This is not a marginal improvement; it is a structural transformation that expands the addressable investor base for premium assets from millions to potentially billions of people globally.

The guide to buying tokenized assets provides specific platform recommendations and step-by-step instructions for investors ready to build fractional positions across these asset classes.

Improved Liquidity for Traditionally Illiquid Assets

Real estate, private credit, and fine art are traditionally illiquid asset classes with lock-up periods measured in years. Fractional ownership tokenization does not magically solve the illiquidity problem, but it introduces the infrastructure for secondary market trading that does not exist in the traditional versions of these investments. Token holders can list their fractional positions on regulated secondary markets or decentralized exchanges, and if a buyer is available at an acceptable price, the transfer settles in minutes rather than months.

The caveat is important: secondary market liquidity for most tokenized fractional products is still thin in 2026. The infrastructure for trading exists, but the trading volumes have not yet reached the levels needed for reliable price discovery and rapid execution on large positions. Investors should view improved liquidity as a long-term structural advantage of fractional ownership tokenization rather than an immediate guarantee of easy exits.

Transparent Ownership and Automated Distributions

Every ownership change, every distribution payment, and every compliance check in a tokenized fractional product is recorded on the blockchain. This transparency eliminates the information asymmetry that has historically plagued alternative investments, where investors relied on quarterly statements from fund managers and had limited ability to independently verify asset performance or ownership status.

Income distributions through smart contracts are automated and proportional. When a tokenized building generates rental income, the smart contract distributes the proportional share to each token holder’s wallet without requiring manual processing by a fund administrator. This automation reduces operational costs and eliminates the delays that are common in traditional fund distribution cycles.

Legal Structures Behind Fractional Ownership Tokenization

The technology of fractional ownership tokenization is only half the equation. The legal structure that connects the digital token to the real-world asset is what gives the token its value and the investor their rights. Understanding these structures is essential for evaluating any fractional tokenized product.

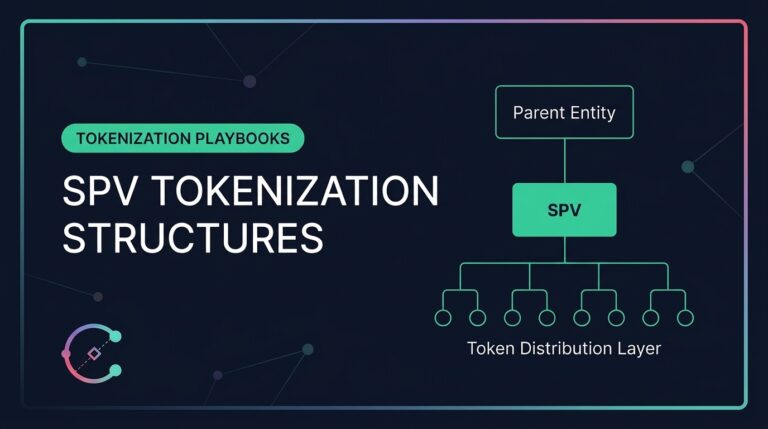

The SPV Model

The most common legal structure for fractional ownership tokenization is the special purpose vehicle. An SPV is a legal entity created for the sole purpose of holding a specific asset or pool of assets. The SPV purchases or receives the asset, and then issues tokens that represent fractional shares of the SPV. Token holders own a proportional share of the SPV, which in turn owns the asset.

This structure provides legal clarity: the token represents equity in a known legal entity governed by the laws of a specific jurisdiction. If the platform that issued the tokens fails, the SPV and its assets continue to exist as a separate legal entity. The choice of jurisdiction for the SPV matters significantly. Delaware LLCs, Cayman Islands exempted companies, and British Virgin Islands entities each offer different advantages for tax treatment, investor protections, and regulatory compliance. The guide to tokenizing real estate covers SPV structuring in detail for asset owners evaluating their options.

Regulatory Classification

In most jurisdictions, fractional ownership tokens are classified as securities because they represent investment contracts with an expectation of profit derived from the efforts of others. This classification means that issuers must comply with securities regulations, which typically include investor qualification requirements, disclosure obligations, and restrictions on advertising and solicitation.

In the United States, most fractional ownership tokenization products are offered under Regulation D (accredited investors only) or Regulation A+ (available to all investors with SEC qualification). In Europe, MiCA and the existing prospectus regulations govern how tokenized securities can be offered. In Singapore, the MAS framework provides a clear pathway for tokenized fractional products that comply with the Securities and Futures Act. The regulatory landscape is evolving, and investors should verify the regulatory status of any fractional product before investing.

Risks and Limitations of Fractional Ownership Tokenization

Fractional ownership tokenization offers compelling advantages, but it also carries risks that are distinct from traditional investments. Investors must evaluate these carefully before allocating capital to any tokenized fractional product.

Smart Contract and Platform Risk

The smart contract that governs a tokenized fractional product is a piece of software, and software can contain bugs. A vulnerability in the smart contract could potentially allow unauthorized transfers, incorrect distribution calculations, or other malfunctions that affect investor holdings. While most reputable platforms conduct independent smart contract audits, no audit can guarantee the absence of all vulnerabilities.

Platform risk is a separate concern. If the platform that issued the tokens ceases operations, investors retain their tokens on the blockchain, but the infrastructure for distributions, compliance management, and secondary trading may be disrupted. The SPV structure provides a legal backstop, but the practical implications of a platform failure depend on the specific arrangements in the token’s legal documentation.

Liquidity Risk

Despite the theoretical advantage of blockchain-based secondary markets, most tokenized fractional products have limited secondary market liquidity. An investor holding a fractional position in a tokenized apartment building may find that there are no buyers at any price during a market downturn. This illiquidity risk is not unique to tokenized products, as it exists in all alternative investments, but investors should not assume that tokenization automatically solves it.

Regulatory and Legal Risk

The regulatory treatment of fractional ownership tokenization products varies by jurisdiction and is still evolving. A product that is legally compliant in one country may not be available to investors in another. Changes in regulation could affect the transferability, tax treatment, or legal status of existing tokens. Investors should understand the jurisdictional framework that governs their investment and monitor regulatory developments that could affect their positions.

How to Get Started with Fractional Ownership Tokenization

For investors ready to explore fractional ownership tokenization, the process begins with education and due diligence, followed by platform selection and portfolio construction.

Step 1: Choose Your Asset Class

Start by identifying which asset class aligns with your investment goals, risk tolerance, and time horizon. Tokenized treasuries offer the lowest risk with yields around 4% to 5%. Tokenized real estate provides exposure to property income and appreciation with moderate risk. Private credit offers higher yields of 8% to 15% with correspondingly higher default risk. Gold provides a hedge against inflation and currency devaluation. Each asset class has a different risk-return profile, and the best choice depends on your existing portfolio composition and financial objectives.

Step 2: Select a Platform

The platform you choose determines which fractional products you can access, what compliance requirements you must meet, and how your investment will be custodied. For tokenized treasuries, Ondo Finance and Franklin Templeton’s BENJI offer accessible entry points with low minimums. For fractional real estate, RealT and Lofty are the most established platforms serving retail investors. For private credit, Maple Finance and Centrifuge provide institutional-grade products with varying minimum requirements.

Evaluate each platform’s regulatory status, smart contract audit history, track record of distributions, and secondary market options before committing capital. No platform is risk-free, and diversifying across multiple platforms reduces the impact of any single platform failure on your overall portfolio.

Step 3: Start Small and Diversify

The low minimums enabled by fractional ownership tokenization make it possible to start with small positions across multiple asset classes and platforms. A $1,000 initial allocation could be split across tokenized treasuries ($400), fractional real estate ($300), and tokenized gold ($300), providing diversified exposure to three asset classes that traditionally required separate accounts, different brokers, and substantially higher minimums.

As you gain experience with how these products work, how distributions are received, and how secondary markets function, you can increase your allocations and add exposure to higher-yield products like private credit. The goal is to build competence with the technology and the products before committing significant capital.

Frequently Asked Questions

What is fractional ownership tokenization?

Fractional ownership tokenization is the process of dividing a high-value asset into smaller digital tokens on a blockchain, allowing multiple investors to own proportional shares. Each token represents a fractional claim on the underlying asset’s value and income, governed by smart contracts and a legal structure like a special purpose vehicle.

How much money do I need to invest in fractional tokenized assets?

Minimum investments vary by platform and asset class. Tokenized treasuries can be purchased for as little as $20 through Franklin Templeton’s BENJI. Fractional real estate positions on RealT start at approximately $50. Private credit platforms like Maple Finance may require $1,000 or more. The low minimums are one of the core advantages of fractional ownership tokenization.

Is fractional ownership tokenization legal?

Yes, in most jurisdictions, provided the issuer complies with applicable securities regulations. In the US, most fractional tokenized products are offered under Regulation D or Regulation A+. Europe’s MiCA framework and Singapore’s MAS regulations also provide legal pathways. Investors should verify the regulatory status of any specific product before investing.

What are the risks of fractional tokenized investments?

Key risks include smart contract vulnerabilities, platform failure, limited secondary market liquidity, regulatory changes, and the underlying asset risks like property vacancies or borrower defaults. The SPV structure provides legal protection, but investors should conduct due diligence on the legal documentation, audit history, and platform track record before investing.

Can I sell my fractional tokens on a secondary market?

Many fractional tokenized products support secondary trading on regulated exchanges like tZERO and INX, or through decentralized trading platforms. However, secondary market liquidity is still developing, and investors may not find buyers at their desired price during all market conditions. Treat most fractional positions as medium to long-term holdings.

The Bottom Line

Fractional ownership tokenization is transforming the relationship between investors and premium asset classes. By reducing minimum investments from hundreds of thousands of dollars to as little as $20, this model opens real estate, private credit, treasuries, commodities, and alternative assets to a global investor base that was previously excluded by artificial barriers of minimum size.

The technology is mature, the legal structures are established, and the platforms are operational. The remaining challenges, including secondary market liquidity, regulatory harmonization, and investor education, are being addressed by a growing ecosystem of issuers, platforms, and regulators working to scale the market responsibly. For investors willing to learn the technology and conduct proper due diligence, fractional ownership tokenization offers a genuinely new way to build diversified portfolios across asset classes that were previously out of reach.

The democratization of investment access through fractional ownership tokenization represents one of the most significant structural changes in retail investing in decades. Subscribe to the Commodara newsletter for ongoing coverage of the platforms, products, and regulations shaping this market.