Tokenized Stocks in 2026: How NYSE, Nasdaq, and Robinhood Are Going On-Chain

Tokenized stocks are moving from pilot to production in 2026, with NYSE building a separate 24/7 venue, Nasdaq filing to integrate tokenization into its existing exchange, and Robinhood launching its own blockchain. The three largest names in US equity markets have each committed to blockchain-based equity infrastructure, and their approaches reveal fundamentally different visions for how stocks will trade in the next decade. This is not a theoretical exercise; these are multi-billion-dollar institutions allocating engineering teams, regulatory capital, and strategic focus to tokenized equity products.

This article covers what tokenized stocks are, why the largest exchanges are building on-chain infrastructure, the specific strategies of NYSE, Nasdaq, and Robinhood, the regulatory landscape that governs tokenized equities, and what this means for retail and institutional investors. For anyone tracking the convergence of traditional financial markets and blockchain technology, the race to tokenize stocks is the most consequential institutional development of 2026.

Table of Contents

This article begins with what tokenized stocks are and why they matter. It then profiles the strategies of NYSE, Nasdaq, and Robinhood in detail. The following sections examine the regulatory landscape, what changes for investors, and the risks and open questions.

What Are Tokenized Stocks and Why Do They Matter?

Tokenized stocks are digital representations of equity securities that exist on a blockchain rather than in the traditional centralized clearing and settlement infrastructure. A tokenized share of Apple, Google, or Tesla carries the same economic rights as a traditional share, including dividends, voting rights, and capital appreciation, but the ownership is recorded on a blockchain ledger rather than in the DTCC’s centralized depository.

The potential impact of tokenized stocks is enormous because equity markets are the largest asset class in the world. US equity markets alone represent over $50 trillion in market capitalization. Global equity markets exceed $100 trillion. If even a fraction of this market migrates to blockchain-based infrastructure, the scale of tokenized equities would dwarf every other tokenized asset class combined. The complete guide to tokenized real world assets places tokenized equities in the context of the broader $25 billion RWA market, but the addressable market for tokenized stocks alone exceeds $100 trillion.

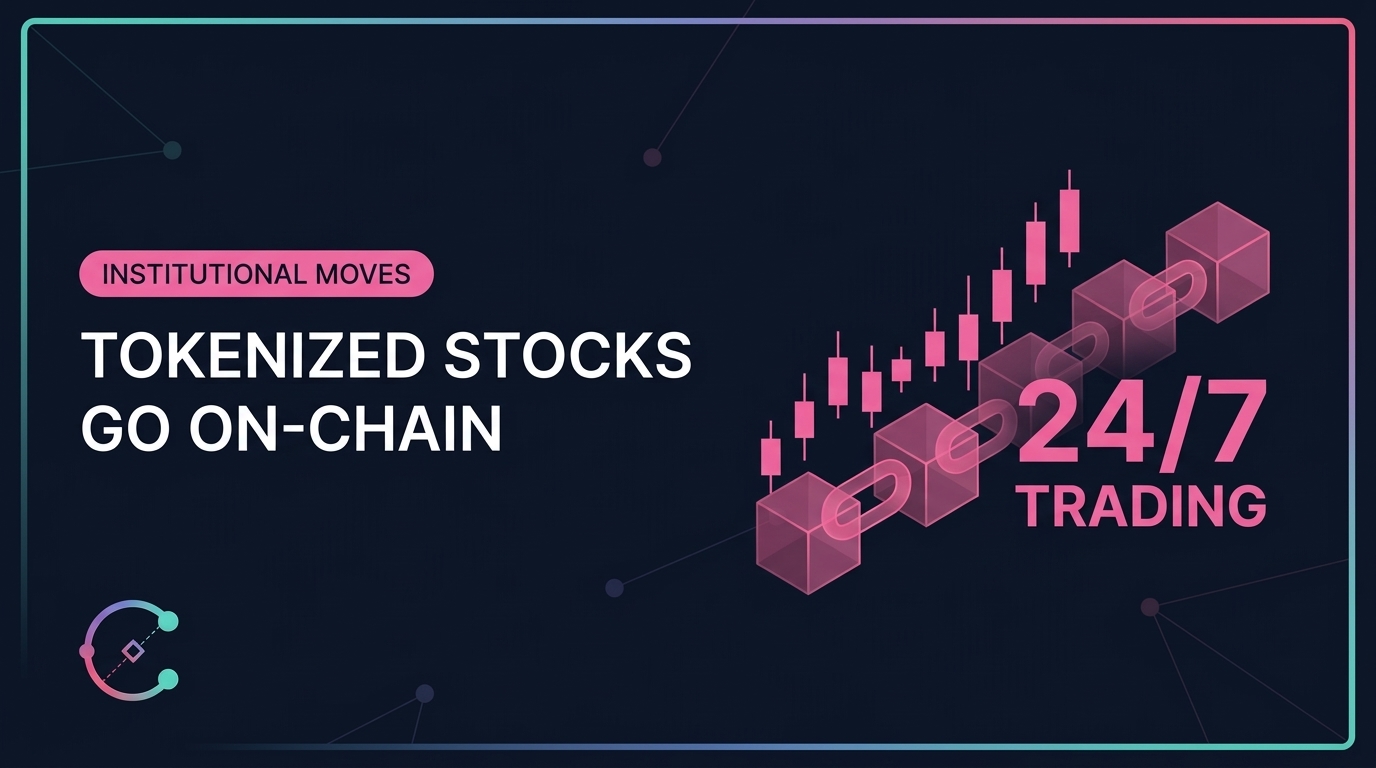

Three structural advantages drive institutional interest in tokenized stocks. First, settlement time compression: traditional equities settle in T+1 (one business day), while blockchain-based settlement can occur in minutes or seconds, freeing up capital that is currently locked during the settlement window. Second, continuous trading: tokenized stocks can trade 24 hours a day, 7 days a week, eliminating the artificial constraint of exchange operating hours that locks investors out of markets during evenings, weekends, and holidays. Third, fractional ownership: blockchain tokens can be divided to tiny fractions, enabling investors to purchase $10 of a stock that trades at $500 per share without the exchange needing to support fractional share infrastructure.

NYSE: Building a Separate 24/7 Venue

The New York Stock Exchange, the world’s largest stock exchange by market capitalization with over $28 trillion in listed company value, is building a separate venue for tokenized stocks that would operate 24 hours a day, 7 days a week. This approach creates a parallel trading venue alongside the traditional NYSE rather than modifying the existing exchange infrastructure.

NYSE’s parent company, Intercontinental Exchange (ICE), has invested in blockchain infrastructure companies and has been exploring tokenization for several years. The separate venue strategy reflects NYSE’s assessment that tokenized equities require different market microstructure, different settlement mechanics, and potentially different regulatory treatment than traditional stocks. By building a separate venue, NYSE can experiment with blockchain-based trading without disrupting the operations of the world’s most important equity exchange.

What NYSE’s 24/7 Venue Means

A 24/7 NYSE tokenized securities venue would fundamentally change the relationship between investors and equity markets. Currently, US stock markets operate from 9:30 AM to 4:00 PM Eastern Time, Monday through Friday. After-hours and pre-market trading exists but with limited liquidity and wider spreads. A tokenized stocks venue that operates continuously would allow investors in any time zone to trade US equities at any time, including evenings, weekends, and holidays.

The continuous trading model also opens the door to real-time settlement. Instead of waiting one business day for a trade to settle, a tokenized stock trade on a blockchain-based venue could settle atomically at the moment of execution. This eliminates counterparty risk during the settlement window and frees up the capital that is currently locked between trade execution and settlement. For institutional portfolios managing billions in equities, eliminating even one day of settlement delay represents significant capital efficiency gains.

The NYSE, Nasdaq, and DTCC tokenized stocks coverage from earlier this year provides additional context on how these initiatives evolved from pilot programs to production plans.

Nasdaq: Integrating Tokenization into the Existing Exchange

Nasdaq is taking a fundamentally different approach from NYSE. Rather than building a separate venue, Nasdaq has filed regulatory proposals to integrate blockchain-based tokenization directly into its existing exchange infrastructure. This strategy would allow traditional stocks listed on Nasdaq to be represented as blockchain tokens without requiring a separate trading venue or market structure.

Nasdaq’s approach reflects a belief that tokenization should be an upgrade to existing market infrastructure rather than a parallel system. Under Nasdaq’s vision, the same stocks that trade today on Nasdaq’s electronic exchange would simultaneously exist as blockchain tokens, with the exchange managing the bridge between traditional and tokenized representations. Investors could choose whether to hold and trade their Nasdaq blockchain stocks through traditional broker-dealer accounts or through blockchain wallets.

Technical Architecture

Nasdaq’s integration strategy requires solving a complex technical challenge: maintaining consistency between the traditional central securities depository (CSD) record and the blockchain record. If a share of Microsoft exists as both a traditional share in the DTCC and a token on Ethereum, the system must ensure that the total supply remains consistent, that transfers in one system are reflected in the other, and that corporate actions like dividends and stock splits are applied uniformly across both representations.

Nasdaq has explored using the Canton Network blockchain and other enterprise-grade chains for this infrastructure, selecting blockchain platforms that offer the privacy controls and performance characteristics that a major exchange requires. The technical complexity of maintaining dual-representation consistency is one of the primary reasons this integration has taken longer to implement than purely native tokenized products.

Regulatory Strategy

Nasdaq’s regulatory filings indicate a strategy of working within the existing SEC framework rather than seeking new regulatory treatment for tokenized equities. By integrating tokenization into its existing exchange license, Nasdaq aims to offer tokenized stocks under the same regulatory protections that govern traditional Nasdaq-listed securities. This approach provides regulatory clarity for investors but may limit the innovation in market structure, such as 24/7 trading, that a separate venue could enable.

Robinhood: Building Its Own Blockchain

Robinhood has taken the most aggressive approach to tokenized stocks by announcing the development of Robinhood Chain, a proprietary blockchain designed specifically for tokenized equity trading. This strategy positions Robinhood not as a broker that lists on someone else’s exchange but as the operator of its own blockchain infrastructure for equity tokenization.

Robinhood Chain represents a vertically integrated vision where the same company operates the blockchain, the trading interface, the custody, and the compliance infrastructure. This is a fundamentally different model from NYSE and Nasdaq, which operate exchanges that other brokers connect to. Robinhood’s approach would create a closed ecosystem where retail investors trade tokenized equities directly through the Robinhood app, with settlement occurring on Robinhood’s own blockchain.

Why Robinhood Is Building Its Own Chain

Robinhood’s decision to build a proprietary blockchain reflects its position as a retail-focused brokerage rather than an institutional exchange. The company already holds over 24 million funded customer accounts, primarily retail investors who are comfortable with the Robinhood mobile interface. By building Robinhood Chain, the company can design the user experience for tokenized stocks from the ground up, optimizing for the retail investor’s needs: simplicity, low cost, and seamless integration with existing Robinhood accounts.

The proprietary chain also gives Robinhood control over transaction economics. On a public blockchain like Ethereum, gas fees are unpredictable and can make small trades uneconomical. On Robinhood Chain, the company can control fee structures, ensure near-zero transaction costs for retail users, and potentially offer features like gasless trading that are difficult to achieve on public chains.

Competitive Implications

If Robinhood Chain succeeds, it would transform Robinhood from a brokerage into a financial infrastructure company. The company would not just facilitate trades; it would operate the settlement layer on which those trades occur. This vertical integration could give Robinhood significant competitive advantages in execution speed, cost, and user experience, but it also creates concentration risk by placing multiple layers of the financial infrastructure stack under a single company’s control.

The competitive dynamics between NYSE’s separate venue, Nasdaq’s integrated approach, and Robinhood’s proprietary chain will define how tokenized stocks evolve over the next several years. Each model has advantages and trade-offs, and the market may ultimately support all three approaches for different investor segments.

Regulatory Landscape for Tokenized Stocks

The regulatory framework for tokenized stocks is still developing, but the direction is increasingly clear. The SEC has signaled openness to blockchain-based equity trading under existing securities law, provided that investor protections, market integrity, and settlement finality are maintained.

SEC Position

The SEC’s approach to tokenized stocks is grounded in the principle of technology neutrality: the form of the record (blockchain versus centralized ledger) does not change the regulatory classification of the instrument. A tokenized share of Apple is still a security, subject to the Securities Act of 1933, the Securities Exchange Act of 1934, and all associated regulations. This means that tokenized stocks must be listed on registered exchanges or traded through registered alternative trading systems, and brokers handling tokenized equities must be registered broker-dealers.

This technology-neutral approach is both a constraint and an advantage. The constraint is that tokenized equities 2026 cannot operate outside the existing regulatory framework, limiting innovations like permissionless trading or global 24/7 access without broker intermediation. The advantage is that investors in tokenized stocks receive the same regulatory protections they expect from traditional equity markets, including SIPC insurance, best execution obligations, and market manipulation protections.

DTCC’s Role

The DTCC, which settles virtually all US equity transactions, is a critical player in the tokenized stocks landscape. The DTCC has been developing blockchain-based settlement infrastructure through its Digital Securities Management platform on the Canton Network. If tokenized equities are to operate within the existing US market structure, the DTCC’s participation in the settlement process is essential for institutional adoption and regulatory compliance.

What Tokenized Stocks Mean for Investors

The transition to tokenized stocks has practical implications for both retail and institutional investors that extend beyond the technology itself.

For Retail Investors

Retail investors stand to benefit from three improvements. First, true 24/7 trading access would allow evening and weekend trading with full liquidity, not the limited after-hours trading currently available. Second, faster settlement means that sale proceeds would be available almost immediately rather than the next business day. Third, enhanced fractional ownership could make it easier to purchase precise dollar amounts of any stock, regardless of share price.

The guide to buying tokenized assets provides context on how retail investors can access tokenized products today, including the early tokenized equity products that are already available through select platforms. As NYSE, Nasdaq, and Robinhood bring their tokenized stock infrastructure to market, the range of available tokenized equities will expand dramatically.

For Institutional Investors

Institutional investors are focused on three different benefits. First, capital efficiency from faster settlement: eliminating the T+1 settlement window frees up billions in capital that is currently locked during the settlement process. Second, operational simplification: blockchain-based settlement reduces the reconciliation overhead that currently requires extensive back-office infrastructure. Third, new product possibilities: tokenized stocks could be integrated into DeFi protocols as collateral, enabling new types of structured products and lending arrangements that are not possible with traditional equity settlement infrastructure.

Risks and Open Questions

Despite the institutional momentum behind tokenized stocks, several significant risks and open questions remain unresolved.

Liquidity Fragmentation

If NYSE, Nasdaq, and Robinhood each operate separate tokenized stock venues, liquidity for any given stock could be fragmented across multiple platforms. A share of Apple might trade on the traditional NYSE, the tokenized NYSE venue, Nasdaq’s integrated system, and Robinhood Chain simultaneously. This fragmentation could result in wider spreads, less efficient price discovery, and increased complexity for investors and market makers. Regulatory requirements for best execution and National Best Bid and Offer (NBBO) consolidation would need to extend to tokenized venues to prevent this fragmentation from harming investors.

Custody and Security

Tokenized stocks introduce custody challenges that do not exist in traditional equity markets. If an investor’s private key is lost or stolen, their tokenized shares could be permanently inaccessible or transferred to unauthorized parties. The irreversibility of blockchain transactions conflicts with the error-correction mechanisms that exist in traditional markets, where erroneous trades can be reversed and stolen securities can be frozen. Solutions like institutional custody providers and broker-managed wallets mitigate these risks, but the custody model for tokenized equities is still maturing.

Regulatory Uncertainty

While the SEC has signaled openness to tokenized equities, the specific regulatory framework for 24/7 trading, cross-chain settlement, and retail custody of tokenized stocks has not been finalized. Regulatory requirements for market surveillance, manipulation prevention, and investor protection in a 24/7 tokenized environment may differ from those in traditional markets. The regulatory landscape for tokenized stocks could evolve in ways that constrain or redirect the strategies that NYSE, Nasdaq, and Robinhood are pursuing.

Adoption Timeline

The timeline for widespread adoption of tokenized stocks remains uncertain. While all three major players have announced their strategies, production deployment at scale may take two to four years. The technical infrastructure, regulatory approvals, market maker participation, and investor education required for mainstream tokenized equity trading represent a multi-year buildout. Investors should view tokenized stocks as a medium-term structural development rather than an imminent change to their trading experience.

Frequently Asked Questions

What are tokenized stocks?

Tokenized stocks are digital representations of equity securities on a blockchain. They carry the same economic rights as traditional shares, including dividends, voting, and capital appreciation, but ownership is recorded on a blockchain ledger rather than in centralized depository systems like the DTCC.

Are tokenized stocks available to buy now?

Some tokenized equity products are available through select platforms, but the major exchange-operated tokenized stock venues from NYSE, Nasdaq, and Robinhood are still in development. Production deployment at scale is expected over the next two to four years as regulatory frameworks and technical infrastructure are finalized.

What is the difference between NYSE and Nasdaq’s approaches?

NYSE is building a separate 24/7 venue for tokenized stocks alongside its traditional exchange. Nasdaq is integrating tokenization directly into its existing exchange infrastructure. NYSE’s approach enables new market structures like continuous trading. Nasdaq’s approach maintains consistency with existing regulatory frameworks.

What is Robinhood Chain?

Robinhood Chain is a proprietary blockchain being developed by Robinhood specifically for tokenized equity trading. It represents a vertically integrated approach where Robinhood operates the blockchain, trading interface, custody, and compliance in a single ecosystem designed for its 24 million retail users.

Will tokenized stocks replace traditional stocks?

Tokenized stocks are more likely to coexist with traditional stocks than to replace them entirely, at least in the near term. NYSE and Nasdaq’s strategies involve parallel or integrated systems rather than complete replacement. Over time, the efficiency advantages of blockchain settlement may drive increasing migration, but the transition will be gradual.

The Bottom Line

Tokenized stocks represent the largest potential asset class for blockchain-based finance, with a total addressable market exceeding $100 trillion in global equities. The simultaneous commitment of NYSE, Nasdaq, and Robinhood to tokenized equity infrastructure marks a turning point for the convergence of traditional finance and blockchain technology. Each institution is pursuing a different strategy: NYSE with a separate 24/7 venue, Nasdaq with integrated tokenization, and Robinhood with a proprietary blockchain.

The practical implications for investors are significant: 24/7 trading access, faster settlement, enhanced fractional ownership, and new product possibilities through DeFi integration. The risks are equally real: liquidity fragmentation, custody challenges, regulatory uncertainty, and an adoption timeline measured in years rather than months. For investors and institutions tracking the tokenized economy, the race to tokenize stocks is the development that will determine whether blockchain infrastructure becomes the default settlement layer for global financial markets.

Subscribe to the Commodara newsletter for ongoing coverage of the institutional moves, regulatory developments, and infrastructure buildouts shaping the future of tokenized equities.